{{item.videoDuration}}

{{item.title}}

{{item.text}}

{{item.videoDuration}}

{{item.title}}

{{item.text}}

In the first half of 2023, investors showed optimism that pushed stock indices to the high end of the year-to-date range, albeit primarily through price gains concentrated in a few large cap tech companies. While strong gains in the broader stock market often lead to open capital markets, interest rate and macro risks have caused a “bifurcation” between rising stock markets and relatively quiet capital markets.

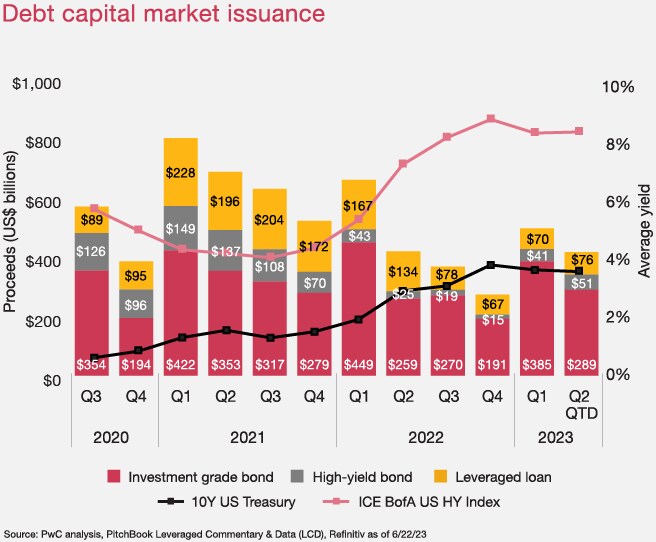

Credit conditions continue to tighten, but issuers have largely been able to push out near-term maturities this year. Still, unresolved questions around inflation and a possible recession remain top concerns.

The US economy entered the second quarter on a weaker footing compared to the previous quarter. Recent data suggest that consumer spending remains positive but is moderating, and increased uncertainty is weighing on business investment planning for the near term. We expect growth to continue to moderate in the coming months as the cumulative impact of Federal Reserve rate hikes, recent tightening in lending standards and relatively elevated inflation limit upside for business and consumer spending.

Business investment remains a significant downside risk. Higher borrowing costs and tighter credit conditions will likely continue to challenge businesses, particularly those in rate-sensitive industries. Capital spending continued to shrink in the first half of the year. Monetary policy uncertainty is high, too. Although the Fed decided to skip a rate hike in June for the first time since March 2022, continued strong payroll growth and elevated inflation mean further rate hikes are likely, per the Fed’s most recent dot plot, which charts projections for the central bank’s key short term interest rate.

The US economy has withstood Fed tightening so far, but economic momentum from earlier in the year is waning, and risks remain tilted to the downside for the remainder of 2023. Even if the US avoids an official recession, economic growth will likely be subdued and many companies could still find themselves in a “profits recession” in the near term.

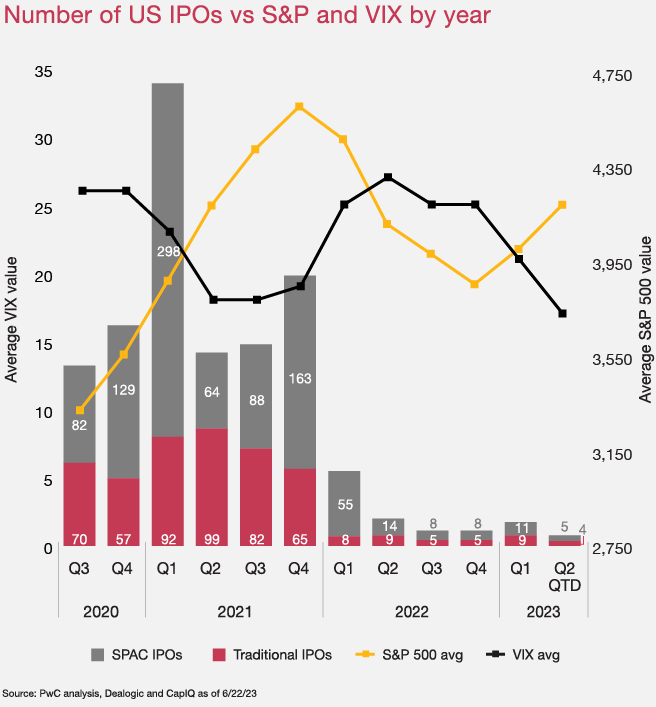

The headline IPO news is that a recent $300 million restaurant offering has opened the IPO window ever so slightly. A few more IPOs are scheduled for the last week of June. Although uncertainties remain, volatility has generally remained on the low side, and both issuers and investors are warming up to current valuations. We believe the IPO backlog may potentially start to clear and the market could start to pick up throughout the rest of this calendar year and early next year.

US debt markets showed resilience during the largest rate hiking campaign since the 1970s and 1980s. While credit conditions and lending standards continued to tighten during Q2, borrowing activity was largely confined to refinancing near-term maturities. There have been some bright spots, including leveraged buyout (LBO) announcements, providing optimism for the back half of 2023, but the high interest rate environment and economic uncertainty continue to serve as headwinds for the market.

“PwC maintains its generally positive outlook for the US IPO and debt capital markets in the long term, providing a strong platform for growth which should see the US through upcoming economic volatility.”

Note: IPOs with deal values of less than $25 million, best efforts offerings, oil and gas royalty trusts, business development companies, pricing on OTC Bulletin Board and OTC Pink Sheets are excluded from this narrative. Data from SEC filings and third-party databases are as of 6/22/23.

To create a clear path forward, you need the confidence that comes from working with a team of straight-talking advisors and actionable insights from a team of dedicated professionals. Find out how we can guide you through each step of the readiness assessment process and beyond.